If your goal is to purchase a home this year, you might be looking for any advantage you can get in today’s sellers’ market. While competition is still fierce for homebuyers, there are ways you can win and secure the home of your dreams, even in a hot market.

Act Early and Save

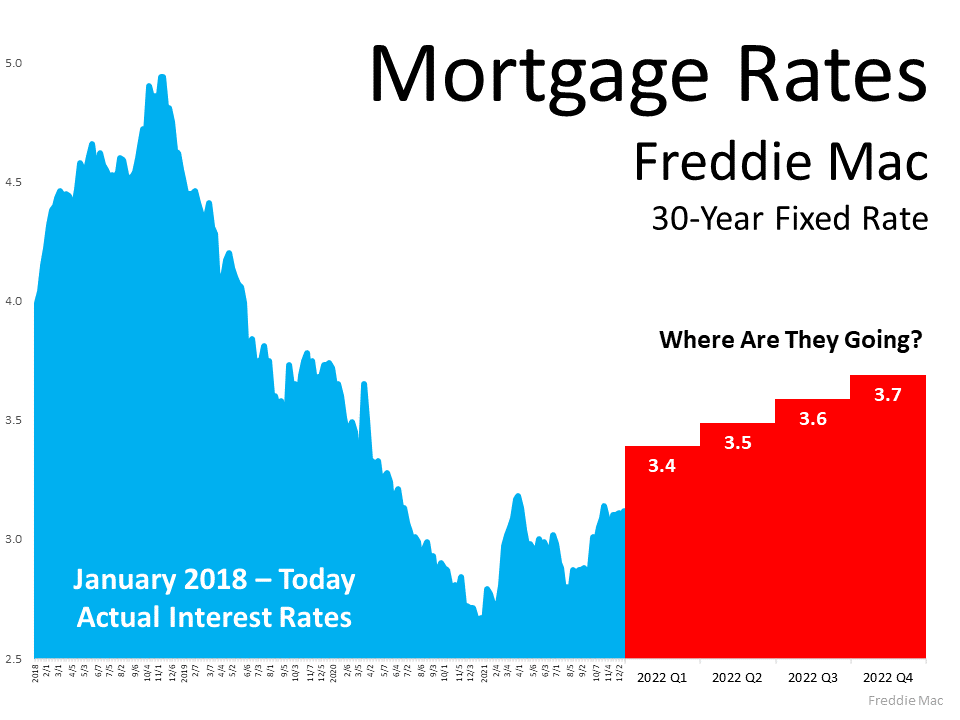

The earlier you act this year, the more affordable your purchase will be. That’s because experts project mortgage rates will rise as we move deeper into 2022. According to Freddie Mac, the average 30-year fixed-rate mortgage is expected to be 3.5% by year’s end. Experts forecast home prices will rise as well.

That means the longer you wait, the more it will cost you to buy a home. Instead, act early and purchase your home before rates and prices rise further. Not to mention, the sooner you buy, the sooner you can experience the benefits of continued home price appreciation yourself. Once you have your home, you’ll be able to watch its value rise, giving you confidence that your investment is a sound one.

Buy Now, Move Later

Keep in mind, with high buyer demand like we’re seeing today, you’ll be competing against other potential homebuyers, which means you need to find a way to stand out. One way to accomplish this is to negotiate with sellers and present terms that meet their ideal needs. Danielle Hale, Chief Economist for realtor.com, explains one lever flexible buyers can pull to entice sellers:

“For buyers with more flexible timelines – such as those making a move from a big city – offering a couple extra months on the closing date could sweeten the deal for sellers who also need to buy their next home.”

In other words, if you’re eager to purchase a home now before it becomes more costly and you don’t have to move right away, you could extend the date of your closing and provide the seller with the time they need to find their next home. That’s a deal that could benefit both parties and help you stand out from the crowd.

Of course, it’s important to work with a real estate professional for expert advice on how to make your best offer. Your trusted advisor knows what’s working in your market and what may appeal to sellers.

Bottom Line

Experts project home prices and rates will increase in 2022. That means buyers who are ready should act soon and find ways to strengthen their offer to meet sellers’ needs. Let’s connect today to learn how you can win in today’s market.

![2022 Housing Market Forecast [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/12/15133751/20211217-MEM.png)